Currently

What Exactly Is a Credit Score and How is it Determined?

Next Up...

What is a Credit Report?

When, Where & Why Should I Check My Credit?

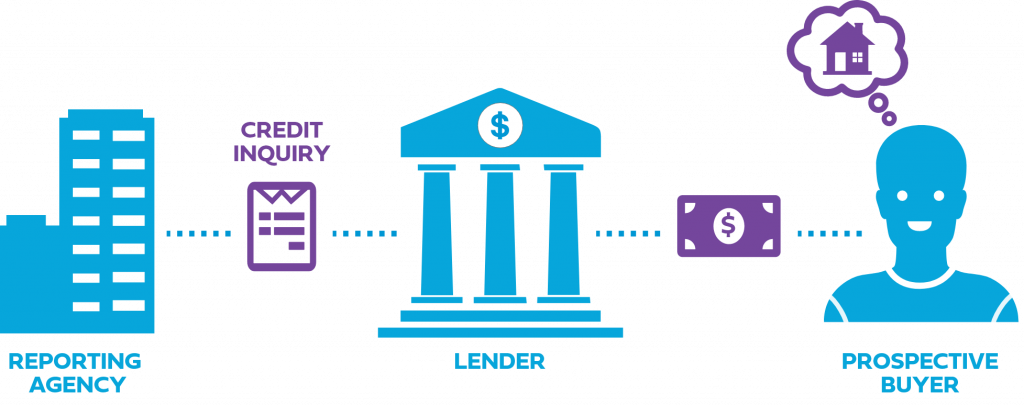

What Is an Inquiry?

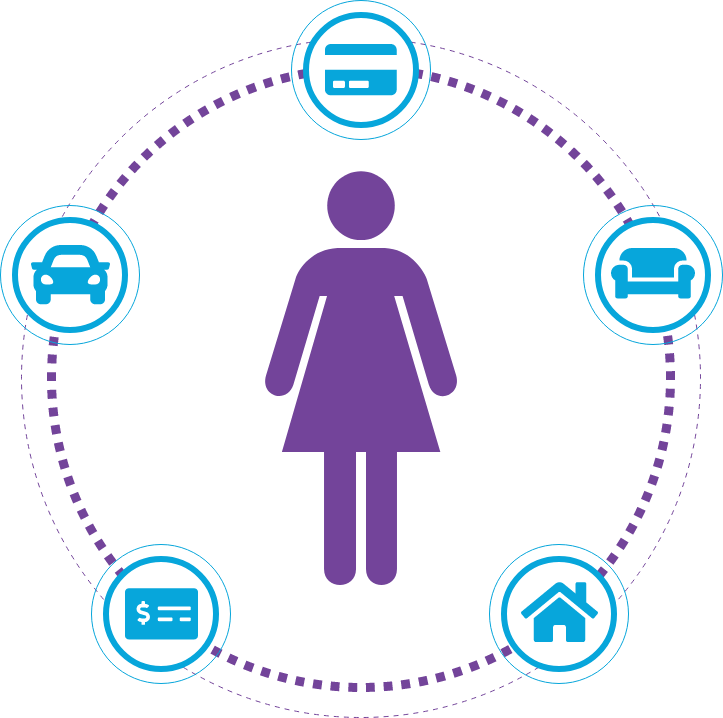

What Is a Tradeline?

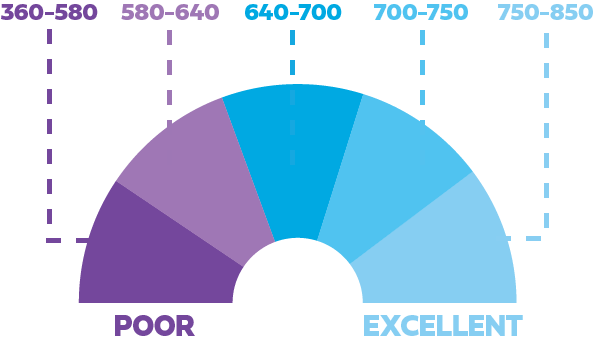

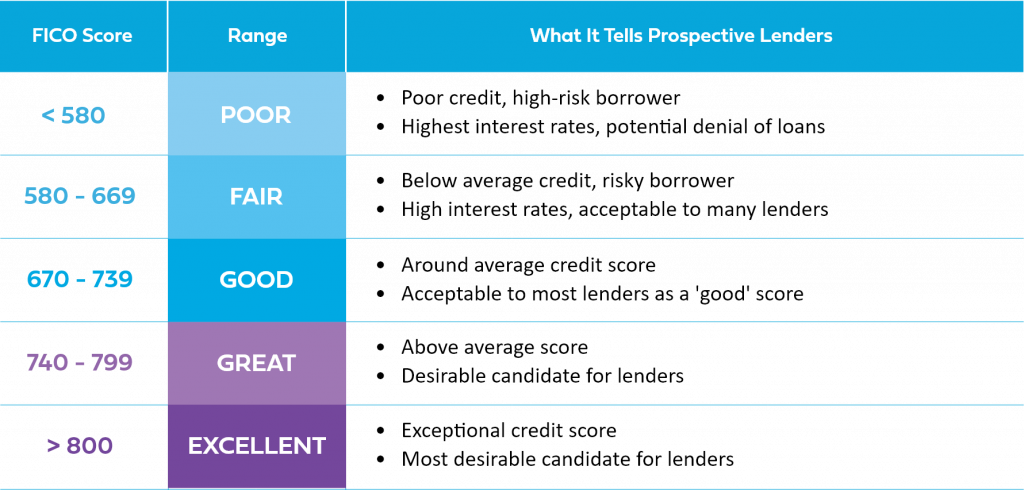

What Is a FICO® Score?

Do Other Scoring Models Exist?

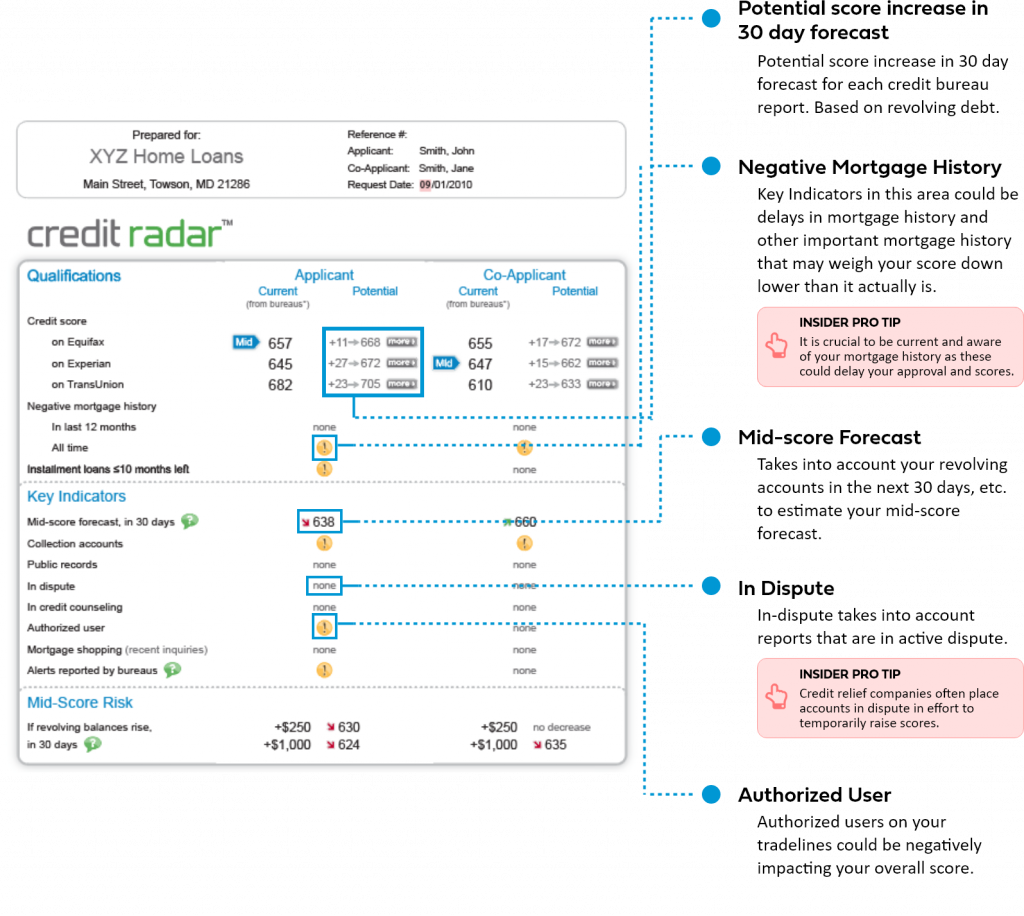

Can My Credit Score Be Improved?

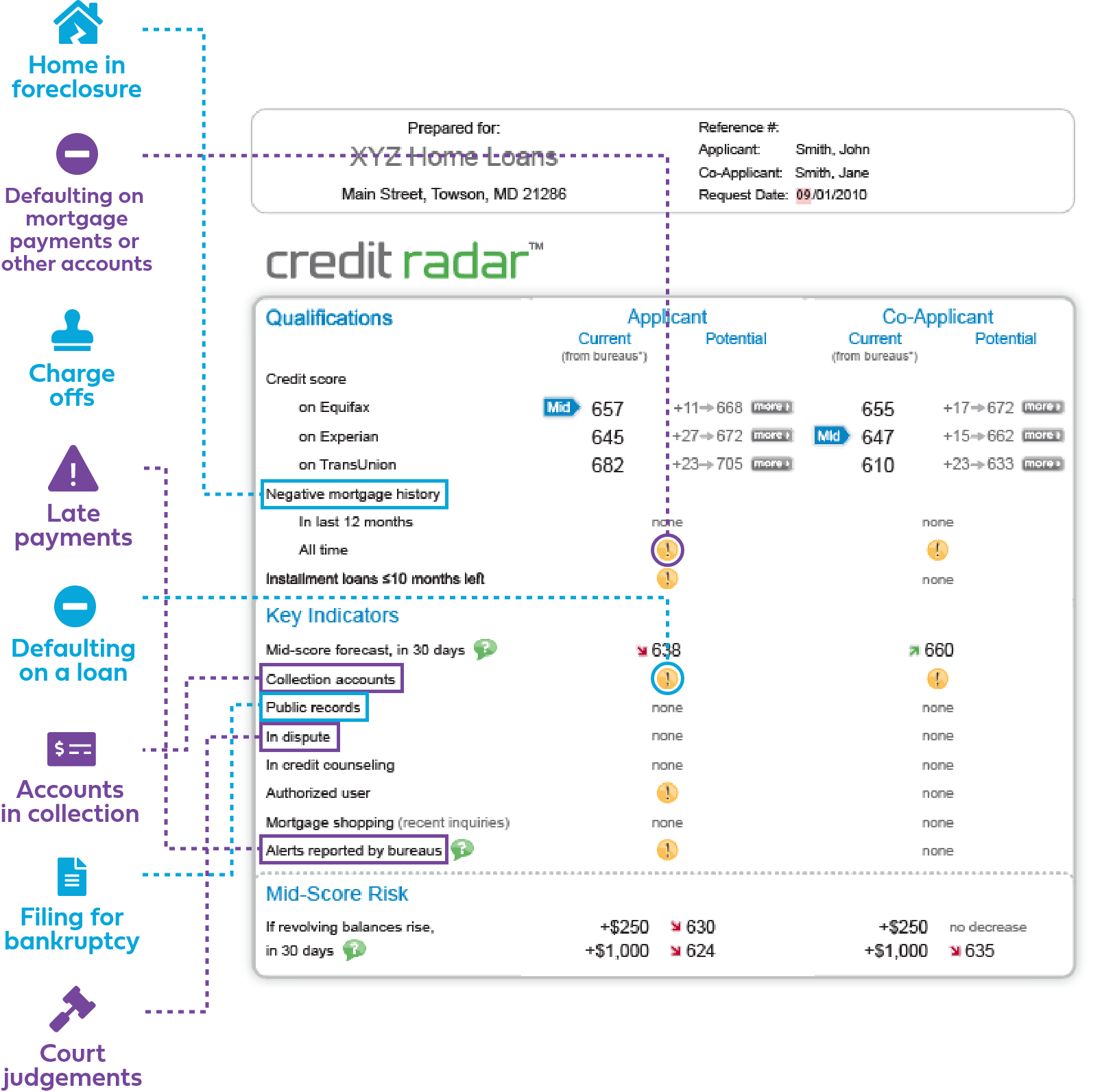

Common Reasons Why Your FICO® Score Is Low

Learned all of

Score & Credit Basics?

Test your Credit IQ with our short, 8 question quiz.