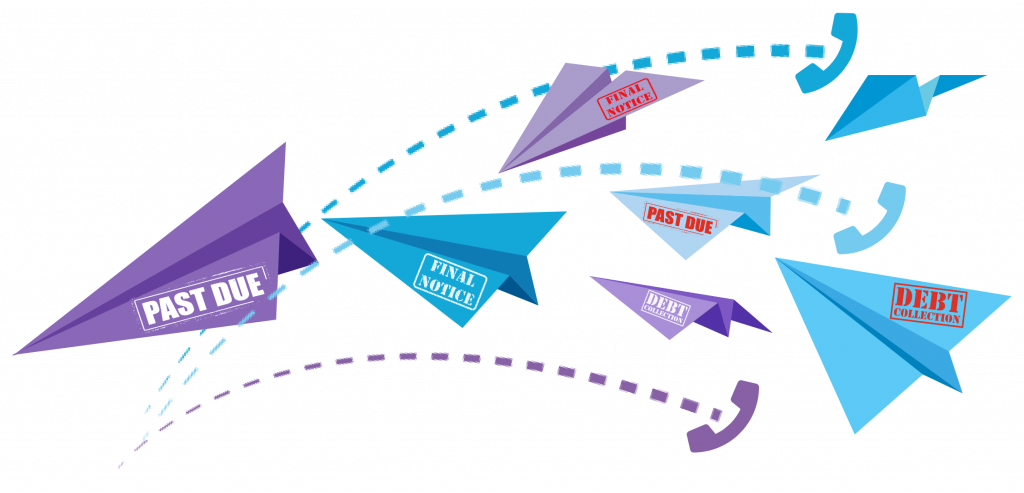

There is an opt-out option, but this does not stop unwanted contact promptly. Mortgage applicants can remove themselves from most marketing programs by calling

888-5-OPTOUT or by registering at

optoutprescreen.com. The downside is that the opt-out process takes up to five days to be activated so it does very little in protecting consumers from the onslaught of trigger leads. Many consumers have reported being subjected to the trigger lead program even after they have opted out.